- calendar_month October 7, 2021

- folder Real Estate News

BY MATT CARTER October 05, 2021

The surge in home prices during the pandemic could fuel the biggest dollar increase in the conforming loan limit for Fannie Mae and Freddie Mac in records dating to 1970.

An increase in the conforming loan limit means more homebuyers will be able to apply for conforming mortgages instead of “jumbo” loans, which are typically harder to qualify for and carry higher interest rates because they’re not backed by Fannie and Freddie.

Some lenders, including PennyMac and United Wholesale Mortgage (UWM), are already offering what they’re calling “conforming loans” of up to $625,000 — even though that’s well above the current $548,250 baseline conforming loan limit for single-family homes in most markets.

Those lenders are betting that home prices kept rocketing skyward during the third quarter, and that they’ll be able to sell the bigger loans to Fannie and Freddie once the conforming loan limit officially goes up on Jan. 1.

Recent home price trends suggest that in terms of raw dollars, the conforming loan limit will make its biggest leap ever on Jan. 1, increasing by more than $75,000. In percentage terms, the increase may fall short of the record 15.9 percent jump seen in 2006.

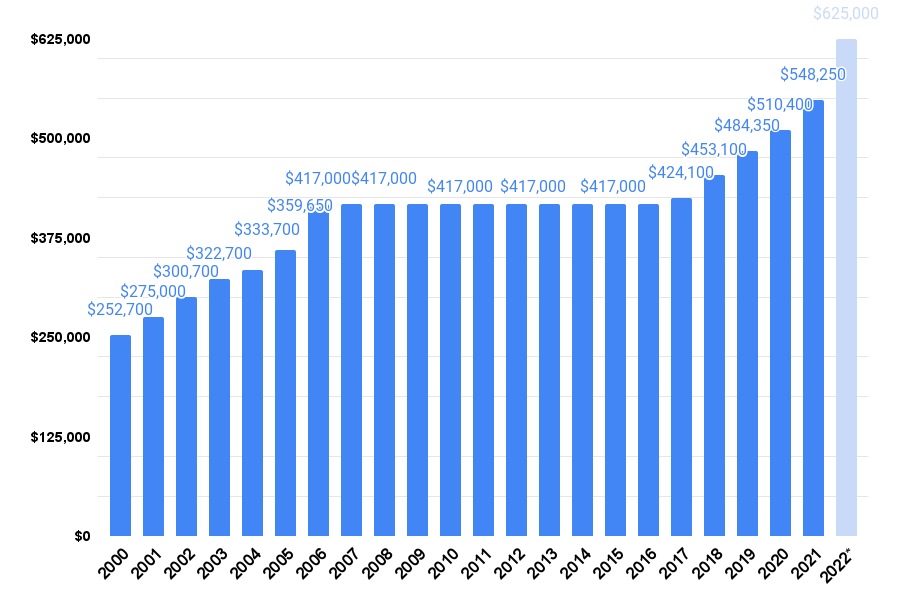

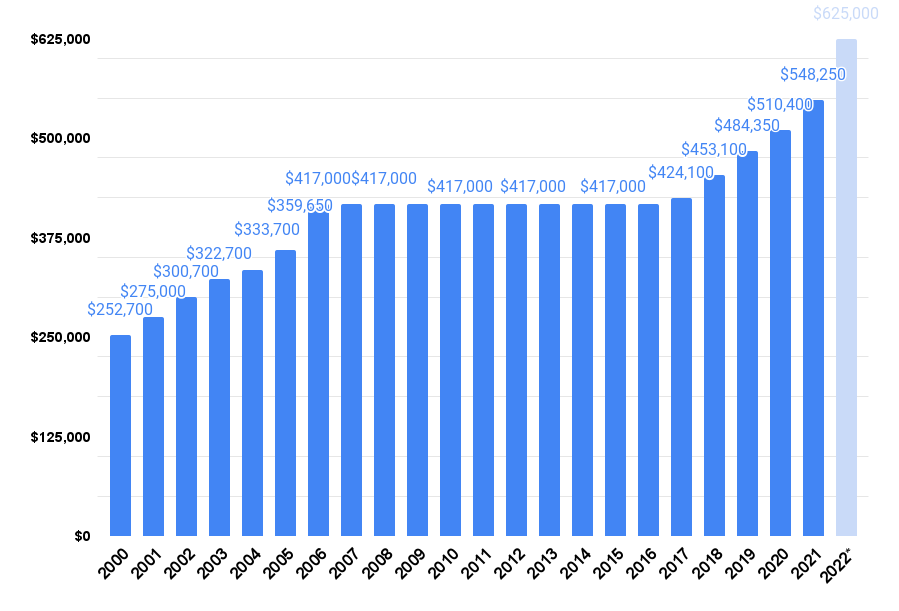

Baseline conforming loan limits, 2000-2021

The baseline conforming loan limit is tied to national average home prices. After the 2007-2009 housing crash and recession, it didn’t go up for a decade, remaining static at $417,000 until home prices clawed their way back to previous heights.

Last November, Fannie and Freddie’s federal regulator bumped up the 2021 baseline conforming loan limit for single-family homes by $37,850, to $548,250. The 7.4 percent increase was based on annual home price appreciation tracked by the Federal Housing Finance Agency’s House Price Index.

In some higher-cost markets, Fannie and Freddie are currently allowed to purchase bigger mortgages based on a multiple of the median home value, up to a ceiling that’s equal to 150 percent of the baseline conforming loan limit, or $822,375. In Alaska and Hawaii, $822,375 is the baseline conforming loan limit for single-family homes, with a ceiling of $1.23 million in the costliest markets.

The FHFA typically releases the conforming loan limit for the year ahead in November, when it publishes the HPI for the third quarter. Even though the official conforming loan limit won’t be known until the third quarter data is available, lenders who are offering “conforming loans” of up to $625,000 seem to be on safe ground.

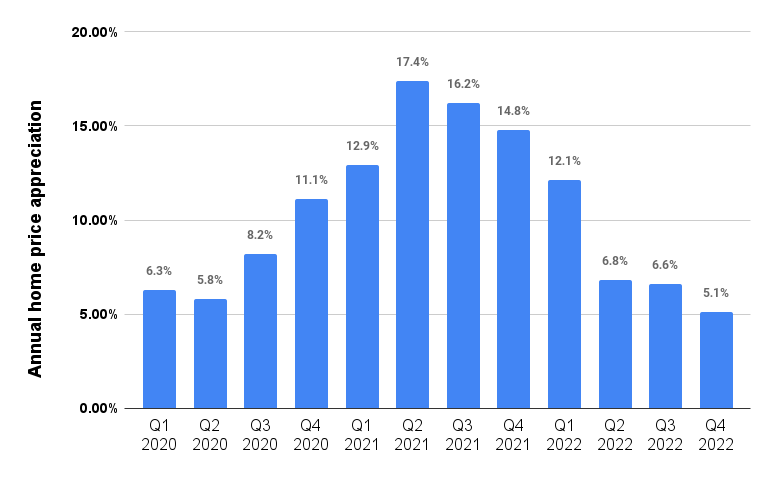

FHFA’s seasonally adjusted, expanded-data HPI for the second quarter shows the index up by 12.83 percent from the third quarter of 2020. That increase alone would be enough to bring the baseline conforming loan limit to $618,570.

Data for the final two months of the third quarter of 2021 won’t be released until Nov. 30. But July’s data showed home prices gaining an additional 1.4 percent — which would be enough to bring the baseline conforming loan limit to $627,230, and the ceiling in high-cost markets to $940,845.

As long as home prices didn’t drop in August and September, the conforming loan limit — which is based on year-over-year appreciation as of Sept. 30 — will be comfortably above $625,000 in 2022. Forecasters do expect home price appreciation to moderate next year, but for now, many markets remain red-hot.

“With the recent run-up in home price appreciation affecting many markets throughout the country, we wanted to step in and provide support for borrowers,” PennyMac executive Kimberly Nichols said in a statement. “This will specifically help those trying to purchase a home or access equity in their property while rates are relatively low.”

PennyMac is offering the following expanded conforming loan limits through the company’s broker and correspondent channels:

- One-unit properties: $625,000

- Two-unit properties: $800,250

- Three-unit properties: $967,250

- Four-unit properties: $1,202,000

In a bulletin to lenders, PennyMac warned that Fannie and Freddie’s automated underwriting systems, Desktop Underwriter and Loan Product Advisor, “will return an ineligible result” when submitting loans that exceed the official 2021 loan limits.

That means “a full appraisal is required for the expanded loan limits,” because appraisal waivers are not allowed with an ineligible decision, the company said.

The expanded loan limits won’t be supported by pricing engines, either, so loan originators need to get rates through the PennyMac Performance Portal (P3), the company said.

In an announcement, UWM said in high-cost markets like Alaska and Hawaii, it will use $937,500 as the baseline conforming loan limit, instead of FHFA’s 2021 baseline of $822,375.

The Pontiac, Michigan-based wholesale lender originally announced on Sept. 30 that it would “honor the 2022 conventional loan limits, ahead of the FHFA November announcement,” and that the “maximum conforming loan limit for regular, one-unit properties will be $625,000.” The announcement has since been reworded to clarify that UWM is adopting “estimated 2022 conventional loan limits.”